We publicize the “special places” that are threatened, and people respond, yes. But we have to face that after 100 years of doing that, the environmental movement that our conservation groups and actions have been at the center of, has protected lots and lots of **special places** but is still not protecting the **ordinary places**.

Protecting thousands of special places, the ordinary places left unprotected

The effect of our organizing has been as if we didn’t know the ordinary places were just as threatened as the special ones, by the same visible and ever expanding encroachment from our economy. Don’t we need to get that straight? Don’t we need to be much more direct in saying that the threats to the special places (that get everyone’s attention) also symbolize the threat to the earth as a whole?

Places like Tucson we haven’t protected

If we do that it could materially change the common goal, recognition that really save the earth we need to **remove the threat**, not just **protect the things that symbolize the threat**. Isn’t that a change in view we need to bring about?

This is a simple way to demonstrate the “dual paradigm view” as a bridge between the abstract complex systems theory and direct study of individual complex systems, to advance our understanding to of the mysterious phenomenon of “emergence”. The article suggested that as statistical systems ecologies generally could never be structurally stable, but did not compare that to systems that rely of “accumulative organizational design” particularly those with “learning parts” as ecosystems systems so often to have rather than “correlated random variables”. The moderator clearly liked this better than my first response not published.

The “dual paradigm view” addresses the dilemma of complexity science that computer models are fine for theory, but don’t really let you study nature. That’s what a way to connect mathematical systems theory with individual systems study addresses. Much of my work of the past 35 years has been on that subject, now recently raised by David Pines’ in a founder’s article for SFRI Emergence: A unifying theme for 21st century science, saying that physics and complex systems science now need a way to study the physical phenomenon of emergence and actual complex systems to progress. My reply to his article Can Physics Study Behavior not Theory, was first posted on Medium.

It’s interesting that with such a number of cross connecting areas of physics being discussed, the ultimate finding technically didn’t answer the initial question posed. That was Robert May’s “question about whether a complex ecosystem can ever be stable, or whether interactions between species inevitably lead some to wipe out others”.

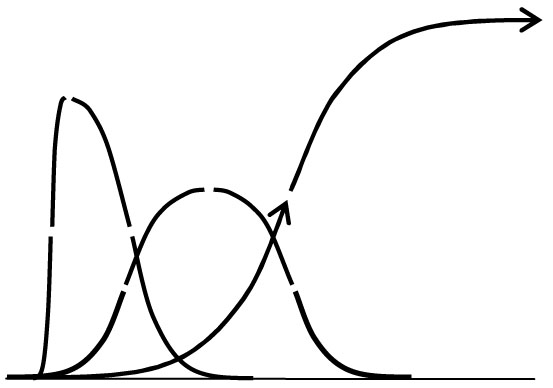

The mathematical analysis of that question and others was limited to “kinds of random growth” and “systems of correlated random variables”. There are also lots of non-randomly behaving systems too is worth considering, and may have been overlooked in answering the basic question. The variety of organizational growth systems that are familiar everywhere in nature display many kinds of growth curves and outcomes, often having an overall appearance of being 1) quite lopsided, 2) quite symmetric, or 3) reaching extended stable states.

note: How the meaning of probability distribution curve shapes (as discussed in the article) differs from the meaning of these individual development curve shapes was skipped in this short comment on the article. Please do bring it up of course if needed. The question posed was about the development of individual ecosystems, and their potential structural stability.

Generic common curve shapes

for the development of organizational systems.

We probably know of lots familiar examples of these from personal experience, where the systems involved are going through progressive organizational change during their periods of acceleration or deceleration. Reversals in curvature don’t always reflect systemic changes in direction for organizational development, but often do though (shown as gaps in the diagram for raising those questions).

The one looking like a TW distribution curve is familiar to all economics and other matters, as a “meteoric rise” followed by “immediate decline”, like many a seemingly fine business plans might experience. The quite unusual thing is this same shape turns up in Gamma Ray burst records too (see image of BATSE 551 #1 below). It raises the question of whether that system (presumably of radiation from black hole collapse) reflects the organizational stages of a system that experiences a “blows out” (like some of our best business plans do) or that of a statistical distribution for correlated variables, or something else?

In any case, just asking that raises the possibility of a bridge between TW correlations and the fates of natural system organization designs, and perhaps a need to consider whether the other kinds of system are available to change the outcome for May’s ecosystems, depending on their design.

Gamma Ray Burst “BATSE 551 #1” – Raw data dynamically smoothed.

For understanding the emergence of new forms of organization in nature, the study of theoretical models seems not to be yielding the kind of useful understanding we so critically need now. What I introduce is a”dual paradigm view”, to address the dilemma, a better technique for learning from nature directly. Computer models are fine for testing theory, but need to be used differently to help us follow the continuities of nature. There is a very big conceptual hurdle, getting mathematicians to study the patterns of nature directly… The physics based method I developed, using models of probability to help locate individual developmental continuities offers a direct way to address the problem Pines raises. It could genuinely offer complexity science a better way to study their actual subject, and couple their theories to actively occurring emergent processes and events. Among other discussions of it on RNS Journal:

Emergence is what we see from cosmic events to the flocking of birds…

David Pines makes a very intelligent assessment, saying in part “The central task of theoretical physics in our time is no longer to write down the ultimate equations, but rather to catalogue and understand emergent behavior in its many guises, including potentially life itself.”

I was one of those who figured out why that would become necessary back in the 1970’s. The behavior of complex systems of equations that permit true emergence will not be knowable from the equations. It’s not just their complexity, but that their emergent properties are emergent and dependent of histories of development rather than being formulaic.

I have also been writing papers and corresponding on the problem very widely since then, and really wondering why I was so unable to get systems thinkers, from any established research community to join me, in studying the commonalities of individual emergent systems. I started with air currents, that generally develop quite complex organization quickly with no apparent organizational input, behave very surprisingly, and seem individually unique.

I actually developed a fairly efficient scheme for studying any kind or scale of emergent system, using the simple device of starting with the question: “How did it begin”. What starting with that question does is immediately shift the focus of interest to considering systems as “energy events”, that you consider as a whole in looking for how they developed. That approach also directs you to look for the event’s naturally defined spatial and duration boundaries, which are highly useful too.

In addition to being fairly productive as research approach, it also made it easy to skirt lots of spurious questions, like “how to define the system”. With that approach your task is finding how the subject defines itself, still looking for a pattern language of structural and design elements to work with, within and around the system, confirming what you think you find.

What I finally arrived at in the 90’s was that the equations of energy conservation implied a series of special requirements as natural bounds for any emerging use of energy. I was thinking that the issue was how nature uses discontinuous parts to design continuous uses of energy, and in working with the equations noticed that the notation for the conservation laws were either integrals or derivatives of each other.

Then one afternoon I just extrapolated an infinite series of conservation laws to define a general law of continuity, and integrated it to find the polynomial expansion describing the boundary conditions for any energy use to begin. It was a regular non-convergent expression, a surprising confirmation of Robert Rosen’s interest in non-converging expressions for describing life, and became very useful as what to look for in locating emergent processes to understand how they worked. I circulated the proof for discussion many times, submitted it for publication a few times and wrote numerous introductions, the following the most recent:

This post is a section of my report titled “Approaching 30 days from the 40th Anniversary” on attending the quite exciting 2012 40th Anniversary meeting on the Meadows and Randers authored Club of Rome “Limits to Growth” study. The excerpt is on the deep reasons why the science, as solid as it still seems to be, isn’t widely accepted. Science is still struggling to find a comfortable way to discuss natural systems whose innovative systems are housed internally, and so largely hidden from view.

___________

I think the real reason the public as well as most of the scientific community is largely ignoring the rather well established hard limits to growth, is that it presents the scientific community a new problem it hasn’t yet learn how to deal with. It has yet to find a good way to make sense of self-designing and self-managing systems, like weather systems, cultures and economies, that have working designs that are hidden internally, displaying organization much too complex and localized to be determined by external forces.

Science is built around identifying how one thing controls another,

not how to study the patterns of uncontrolled systems and how they became designed to work by themselves.

So science is naturally somewhat lost in discussing how they work, having no model for what are better described as “opportunistic” than “deterministic” systems. Though both climate and economies display highly inventive systems, they do still necessarily operate within what traditional science can define as their natural bounds. Climate is still fundamentally a complex pressure-temperature behavior, of unchanging deterministic processes following fixed laws of science.

Economies though, are able to be far more creative, and move the boundaries of what is possible by innovative design, much further than the push and pull forces of the weather can. It has given traditional science very little to anchor reliable theory on, except as in the Limits to Growth study, fixing boundary conditions and experimenting with multiple options. Still, because economies do display deeply creative behavior, constantly inventing new ways to use energy as a normal rule, that natural science still lacks a widely accepted way to study them as natural systems, adds uncertainty for others to what anyone might say about them.

Constantly inventing new organization is just what natural systems ‘do’. It lets economies as well as ecologies create new kinds of organization and uses for their energy resources, making formerly useless things highly profitable often enough. Using the profits as returns on energy investment to grow by building more innovations. It’s complicated by not being a ‘numeric’ process, though we can see it through our measures. It’s an “organizational process”, of fitting complementary parts together, more amenable to study as a “pattern language” of “design elements” than equations.

The rigid limits of any mode of productivity still do exist, of course, but as limits of the organizational processes science has yet to find a way to study. Those limits are still determined by the earth and the organization of the internal and external systems that any innovation depends on, but with each new innovation there are new unknown limits. It leaves a stubborn problem for traditional scientific prediction. What seems to work better is a language of observing such systems to see when their own organization is being stretched.

Natural systems generally link individual units of organization in an open rather than deterministic environment, each with its own internal organization that emerged during its own development, creating a serious mis-match between the natural design and the information an observer could collect, and with the kinds of behaviors that can be emulated by equations.

That big problem for science also makes a big and very fascinating subject of study, that science has quite generally not realized is there, having avoided the study of self-designing and managing systems in general. Self-designing ans managing systems not only seem to develop by themselves, but to have their “works” hidden internally within the boundaries of their design, as an individual system maintaining internal organization for responding to external systems, like we see in living systems as a special case in point. Continue reading Can science learn to read “pattern language”…?→

This is as simple a story of this amazing change in our economy. What happened is that the economy ran into increasing resistance from the environment. The inequity came from how that slowed down wage growth more than the investment income growth. Below are two simple ways to understand the natural cause of the problem, that were posted to the discussion on NPR.org today.

Without a major rethinking of our growth strategy it really can’t be fixed, not by this congress or any other, as it’s “natural”. The problem is our growth strategy is running into ever increasing natural “drag” and “resistance”, that affects labor more than investment earnings.

See also my recent articles:

“Kepler” – a great story of student discovering how to understand the big picture

“a Whole Systems view – Piketty’s “r > g” – Relating it to Thomas Piketty’s book on global inequity

Comment 1

You never seem to be allowed to talk with the people who know why wages began stagnating in about 1970. There are very specific natural reasons.

Keynes predicted it. I’ve detailed it to the Nth degree. It’s a perfectly common problem in many ways. The simple word to call it is just “drag”. The economy is meeting ‘drag’.

You experience drag as a kind of resistance to what you were doing before. There are millions of kinds. The evidence of very numerous kinds of resistance increasing at accelerating rates more or less all together at once, for the whole system… goes back about a century.

None of you seem to understand that economies are designed to run themselves. Nobody mentions that in the media either, or even the smart pundits. I guess it’s because the people you hear talking about it are really just competing for attention or promoting their ‘angle’ or don’t know any better.

The real situation is that economic growth is stimulated by the money earned by investors being added to the pool of money for creating more businesses. So with growing investment you get a growing economy,… and it’s markets expand, using more and more of every resource they can find on earth…, till something goes wrong.

When things are going right, like in growth periods up to 1970, the incomes of the rich grow faster than anyone else’s, *but* there’s enough left over to “trickle down”, so the incomes of everyone else keep growing too, just a little slower than for the rich. After ~1970 the relative rates started spreading apart further and further, till most people don’t even increase their incomes as fast as inflation…

One of the things going wrong is the economy is running into natural resistance, from its growth having changed the world, to make it less bountiful. The economy is slowed down by needing to use more costly resources, from increasing complications of regulation, increasingly complex designs and teamworks needed to get anything done, increasing costs of global competition and conflicts between industries demanding growing shares of diminishing resources.

What’s most obvious if you look at the data is that after 1970 growth continued for the richest and not for the rest of the wage scales. I think there were all the above problems creating drag for the whole system, effecting the productive economy and lower incomes the most, and the people at the top the least. People of course saw that was where to make the money, and those that could went in to investing to use money to may money that grows without actual work. Investing is a kind of ‘work’ where the more money you have the more you earn, without any actual “labor”. So, that kind of earning really took over.

There’s lots more interesting to say, looking at the economy as I do as self-guided system driven by people’s choices and the capacities of the earth the find to use and use up that way. The bottom line, though, is that there’s too much unproductive investment.

The one and only way to reverse that (other than “resetting” the game with gigantic financial collapses) is for the wealthy to *spend* their earnings rather than *accumulate* more unproductive investments. JM Keynes actually proposed that would be necessary, as the solution for this very problem, that he saw as likely to come up in what he saw as the relatively near future, from the 1930’s.

I’ve written lots on it myself, but it’s “unpopular” because you need to look at the financial implications of our having been running into increasingly resistance to growth as approaching limits, for 50+ years…. That subject was made socially “taboo” in discussion groups not unlike this one all over the world in the 70’s, in case you don’t know about that. And the whole world went to sleep in total denial of there being limits to growth or anything eles, population too.

…and the laws that move you from maximizing power to maximizing resilience.

Like many young college women Kepler awoke that morning with other things on her mind than the project she had planned for the day. She had been dreaming about how she loved her drawers of personal things, in colorful piles, neatly rolled, in little bags and folded, each in its own style and fit together. Maybe she would become a “collector”, she thought, they gave her such a thrill. How nature was “quite a collector” too fascinated her too, creating all the natural world’s very special arrangements, with everything having it’s own individual home, utterly improbable in such number and variety, and so highly organized and grouped with fitting parts everywhere.

She’d also been told that lots of scientists thought nature’s patterns came from a natural law of energy, that everything sought to maximize its power, which honestly, just made her wrinkle her forehead… She did not know, of course, but thought there was something hidden in the magic of how things in nature so often yielded to each other, an obvious secret to how things come to fit so closely. So she quietly thought perhaps that seemed at least or was perhaps even more important.

What she had planned to do that day was use her old graphic calculator from high school, to do an experiment in rewriting the history of the economy, laughing as she said it that way. Could you show an economy as being responsive, seeking to get along, rather than just getting more and more aggressive in looking for, in the end, how to get in ever bigger trouble? What would it be like, she wondered, if people could be responsive as a rule. The idea had come up in reading that the climate change scientists, the IPCC, had said we needed to reduce world CO2 production to half what it was in 2010. It was only recently in fact that the world economy had been below that, and now everyone was saying we had to go back but probably couldn’t. She felt she had all the facts, though.

So she had the idea to just…

– totally redraw the history of ever growing CO2 – to show mankind as being responsive to the approach of climate change

She didn’t get it to work till quite late that night, but it worked! What she had of course been thinking about, and felt that anyone who mattered constantly worried about behind every other subject, was the strange continual way the human society was so energetically trying to destroy its own future. The evidence could not be more clear, with the ever faster consumption of everything useful on earth, that an economy maximizing its growth unavoidably does. Anyone can plainly see that happening, as climate change keeps accelerating faster than expected. Everyone hears about the ever increasing loss of natural species from disrupting ever more natural habitats too, and the impossible debts nations have accumulated making their decision making impossible, and so many other disturbing things.

It wasn’t a “debate” to her. It also wasn’t her “cause” either. She also did not really see it as her job to change other people’s minds. It was just something she personally needed to know, about her own life, and whether it could be meaningful. Continue reading Kepler→

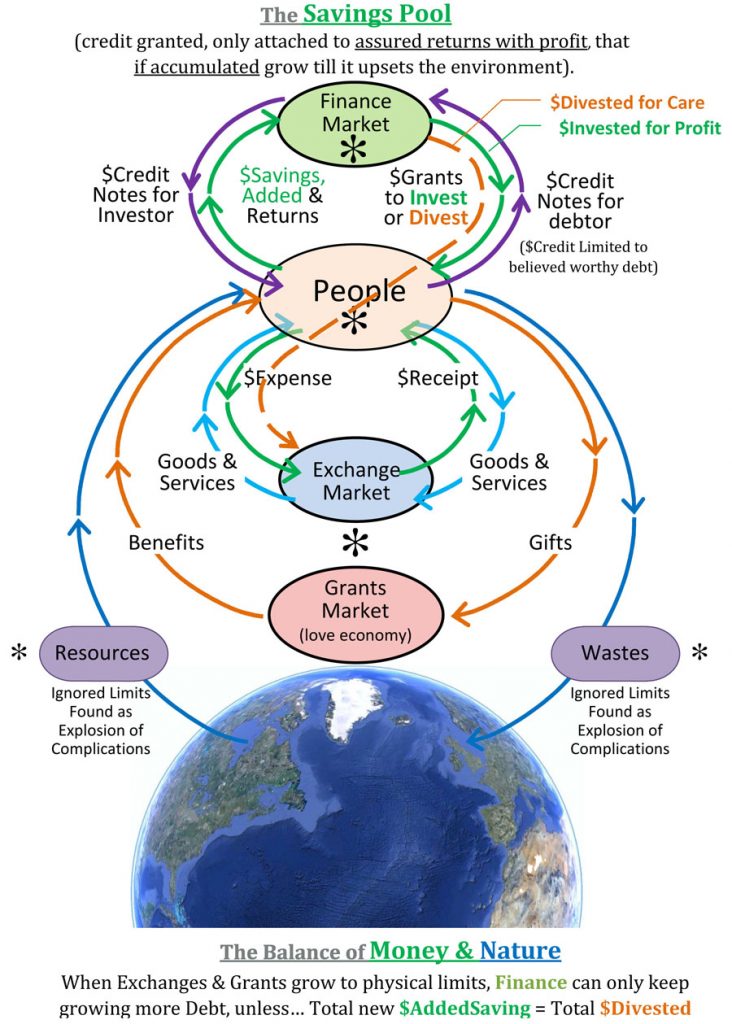

The trick is that there are two ways to do that. 1) you can add the money you earn from investing money, to increase what you then reinvest, so it multiplies what you take out (to put back in to take out more), or 2) you can use the money you earn from investing to take care of the things your investments built, or anything else.

Some links to other discussions of it are below, and a request for your comments.

Here’s an excerpt from a Facebook exchange. It goes another step in explaining why this particular difference, using profits from investments to build more and more to profit from, or to care for things, causes major confusion in our modern world. We want both, definitely want both! But they’re mutually exclusive and there’s a kind of “deadline” for making a choice that most people, for some reason, would quite prefer to ignore, as if there was no choice to be made

______________

Jessie Phyllis Rose HenshawSpeaking of money… Doesn’t “inequity” come from the wealthy PUTTING MONEY IN TO TAKE MORE OUT (and so to then put even more in to take even more out)? It *seems* fair… WHEN IT STIMULATES FASTER GROWTH, but that isn’t determined by people, but nature is it?

Helene FinidoriThat’s a great statement Jessie. Could we say faster extraction? Also well I guess many want to put some input into something to get a little out (think of mom and pop savings for retirement). The question is to what limit… Could you plug this somewhere on the pattern language site? Because this is typically the ‘more of the same’ that any new solution would like to avoid…

Jessie Phyllis Rose HenshawYes, I’ll put it there. If I’ve finally said it so people would ask questions, like you just did, then I’ll need help expanding on it so I don’t lose people with the details. The issue is *the balance* between the strains on nature and people and the increasing scale of the whole system.If it were a policy decision, it would be to “stop counting on an ever bigger windfall from the future”. The default way to do that would be to ask everyone to plan for a future of “pay as you go” and people with large investments to use their profits, primarily, to heal the strains on the commons instead of continuing to invest their profits in expanding our burdens on it. Mom & Pop’s savers tend to do that anyway, so no policy required!

__________________

Please add comments on what puzzles you about it, your creative questions or observations. What should we do with our money. The earth commons we are part of has the profits from a hundred trillion dollars to think about how best to invest, and all the people who expect it to just keep multiplying forever to buy in on the plan too!

“Pattern Languages” give meanings to patterns in nature, theories, relationships or experience, but we often don’t know quite how. Like, we all tend to consider our own conscious view of things to be the world we and everyone else all live in… even though everyone is making up their own view of that. That kind of real world doesn’t fit into any simple explanation, of a world in which everyone is seeing a world that is in large part a reflection of themselves. It creates a lot to untangle.

One of the fascinating scientific subjects I research is how human understanding comes from narrative. Without getting too technical, narratives about relationships, environments and culture change issues come from people “observing the flows” of the natural processes, the flows by which those changes in our world take place. The basic starting point, then, is having some way to observe those flows. No awareness of the flows, *no story*!

This is such an important thing for combating our alienation from the breakdown of traditional cultures, really all around the whole. It’s quite an unfortunate side effect of the great eruption of wealth in modern times, and the ever more intense global competition fostered by the world economy doing it. A small part of how it disturbs our ability to tell stories about what’s happening to us in yesterdays post What is a “rights” agenda, with ever increasing inequity?

Mining live stories from big data is way to build human understanding

Use maps of natural silos of conversation to find who you need to talk to and how!

I ran across five wonderful examples this week alone, of ways to bridge the enormous cultural and intellectual divides the keep us from arriving at a common understanding of what to do with the earth. My topic yesterday saw how an economy structured to produce both ever increasing complexity, inequity results in the breakdown of traditional cultures and ways of knowing, a loss of stories for giving our lives meaning. Learning to see the problems can also be used to find solutions too, of course, the main one here perhaps just learning to see what we’er doing to ourselves. The thought process leads to seeing what strategies are failing us is not so different from that used for discovering promising new ones.

One identifies where the cultures that guide us lose track of what’s happening to them. The other discovers exposes the flows of events in a way allowing us to create the new stories that will matter in our lives. It’s how all human rights are achieved, by recognizing them as the clear story that beings order to a disruptively changing world, recognizing how nature connects the dots, letting us frame not just “good stories” but also “true stories” about finding a sound new path.

The practicalities of recognizing “what’s really happening” so we can use our values to fashion the stories telling us what to do will mostly not need a lot of big words and shiny promises. You can do it with “big data”, even if today its main use seems to be for controlling personal data to make growing amounts of money from deny people their individuality. You can also us it to mine the data world to pick up clear signs of whole new cultures emerging you’d otherwise never be aware of, for example. Having ways of visualizing the eventfulness of change globally, on many dimensions, would be a very *different* kind of “news feed”, a true globally holistic “news feed”.

Every community could study the eventful flows of changing relationships, personal, cultural, economic, ecological, that matter to it, rather than just listen to media largely composed of chattering entertainers and politicians after money and power. If a way of mining data for signs of events could show people what’s really happening to their world, and that became the the talk of the community, everyone could participate in shaping the news and the new stories about our human rights tell us to do. It would give the media a real story to cover too. The practical job to make that possible, though, is more like science than philosophy. It’s to learn to recognize that eventful change comes from the emergence of new forms of organization, that generally begin with a viral burst of development, that energize whole systems, altering the balance and roles withing their environments, like organisms that growth from a seed to build new natural capital or flame out.

Shown as the general stages of growth for a new form of organization, from novelty to maturity

Examples

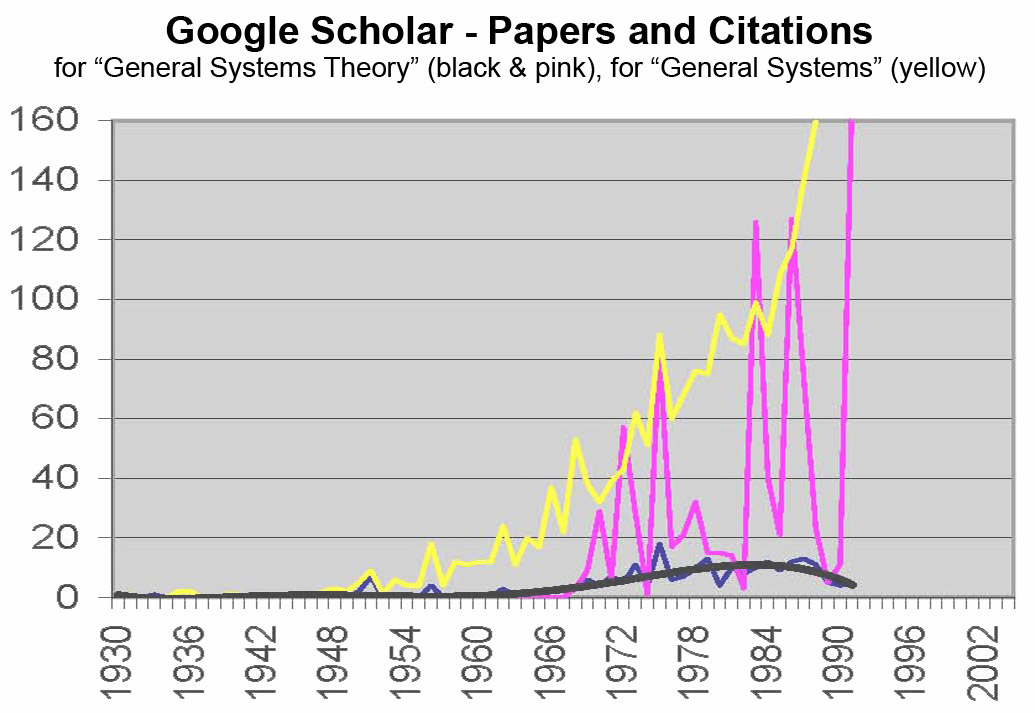

1. – Changes in Word Use – I am not an expert in semantic analysis, fundamental changes in word use, particularly if following a clear developmental pattern generally do indicate a change in the world of people and their way of speaking about it. Developmental changes in word usage expose important cultural experiences of the people writing the text. I’ve used comparisons of the Google histories of word frequencies obtained from scanned libraries of books, their “Ngram” tool. I’ve also used the histories of word use in magazines, newspapers and even Google Scholar, such as to identify

Along with the various other “story mining” methods discussed in the introduction to my scientific method for mining the stories of natural change processes, and method of interpreting them:

Learning to read the eventfulness of our world – People who have some personal experience with the environments in which these explosive changes took place, as eruptions of new organization for those worlds, these documented records of the shapes of their stages of growth provide rich reminders and new challenges to imaging what was really going on to produce the new environments the created.

Papers on “General Systems”(yellow), Papers and Citations for “General Systems Theory” (black & pink)

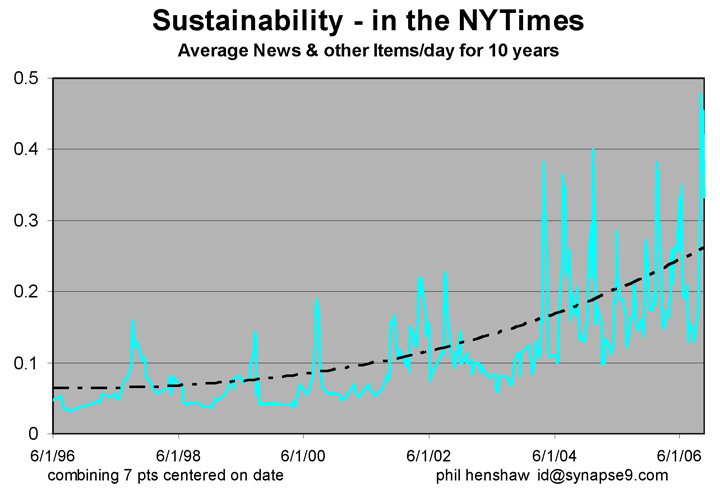

“Pop Corn” flurries of articles on sustainability as the subject emerged in the NY Times, and Accumulative trend

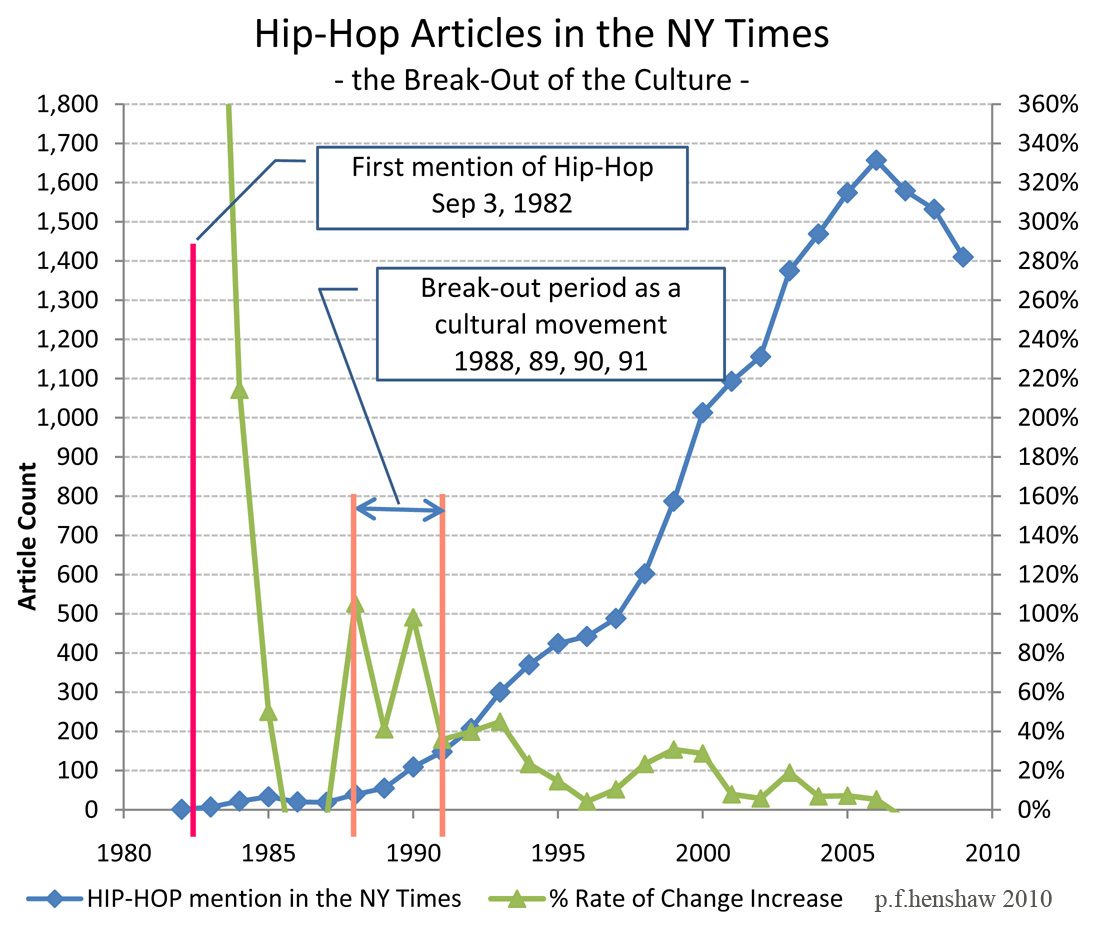

The 1990 beginning of the big eruption of mentions of Hip-Hop in the NY Times also coincided with the historic sharp decline in NYC crime rates, culture change as kids changed who they looked up to.

Use of “complex” followed growing economic complexity up to ~1960, when we appear to have either lost interest or the ability to keep up, with the fast increasing complexity of our world.

Today one might also use Twitter and other social media, and also collect data on product and book sales and lots of other sources. Of course, the sources would vary considerably from country to country, but the method would be the same. What’s important is for the text or numeric data being scanned for “natural coupling” be “neutral” and not influenced by the subject being explored.

What might be possible, putting it all together, is to identify natural cells of social relationships and their interests, cultural “silos” of relationships identified by their ways of using language, in real time. There are security questions whenever new kinds of information are made available, so such maps should be abstract. The most valuable feature of such a “map” of connections, though, is the ability to then see who’s NOT connecting, the isolated constituencies.

You’d see what conversations are intense in one group and missing from another, say between Twitter and the local newspaper as one possible divide., defining two communities with differing values and interests. That would be a great tool for understanding a society, and a great tool for social activist groups, letting them see how to stop “preaching to the choir”, for one example. It wold also give them insight into the words and interests of the groups they need to connect with, but hadn’t known how. Seen that way it’s a “partnership tool”, allowing people to see through the silo walls just enough to make some connections.

It helps to look at the long term trends to recognize the long term pattern.

In a world of ever increasing inequities we clearly can’t sustain a real “rights agenda”. Even the strongest of moral commitments is no match for a world economy which in a lasting physical way, is systematically splitting apart.

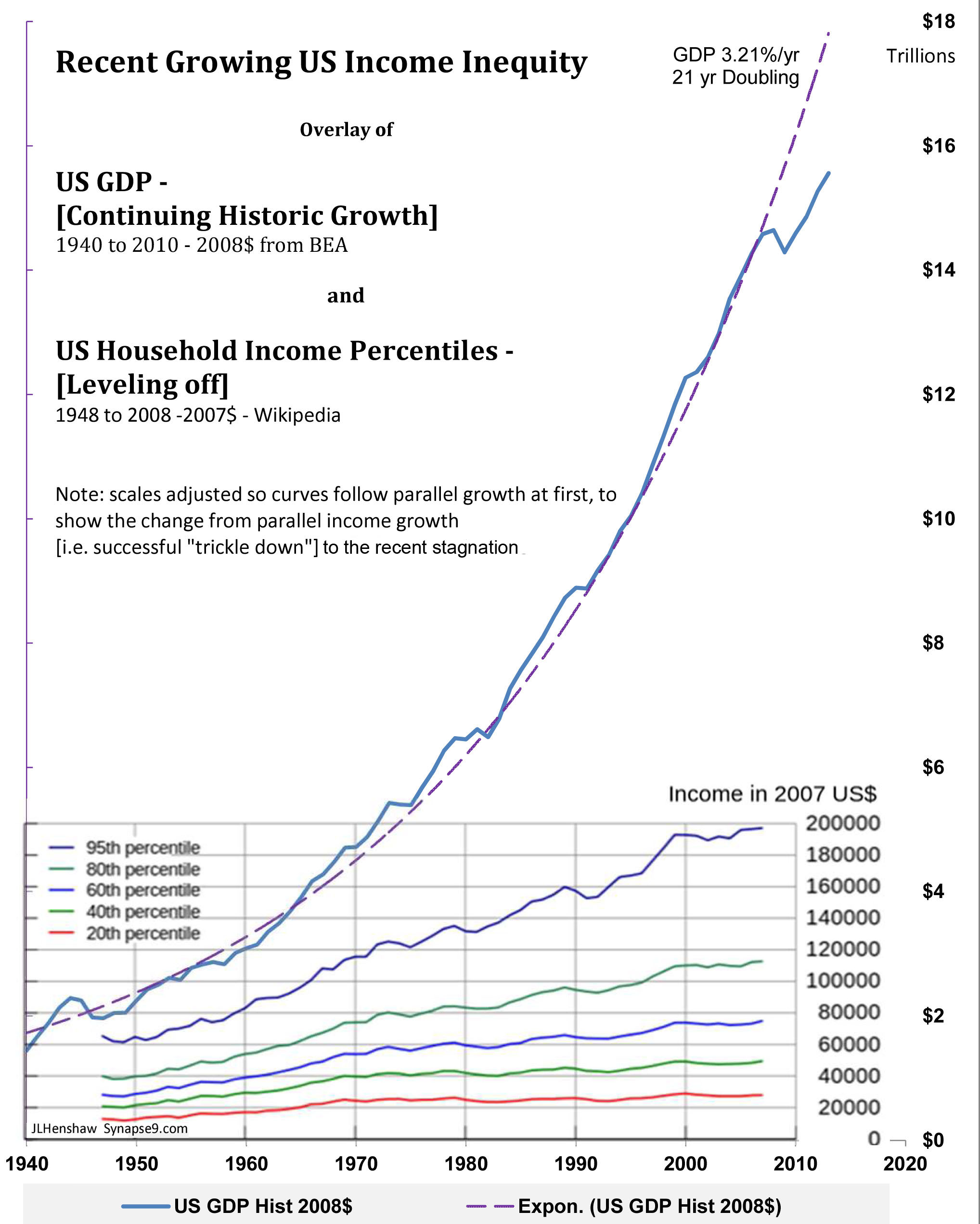

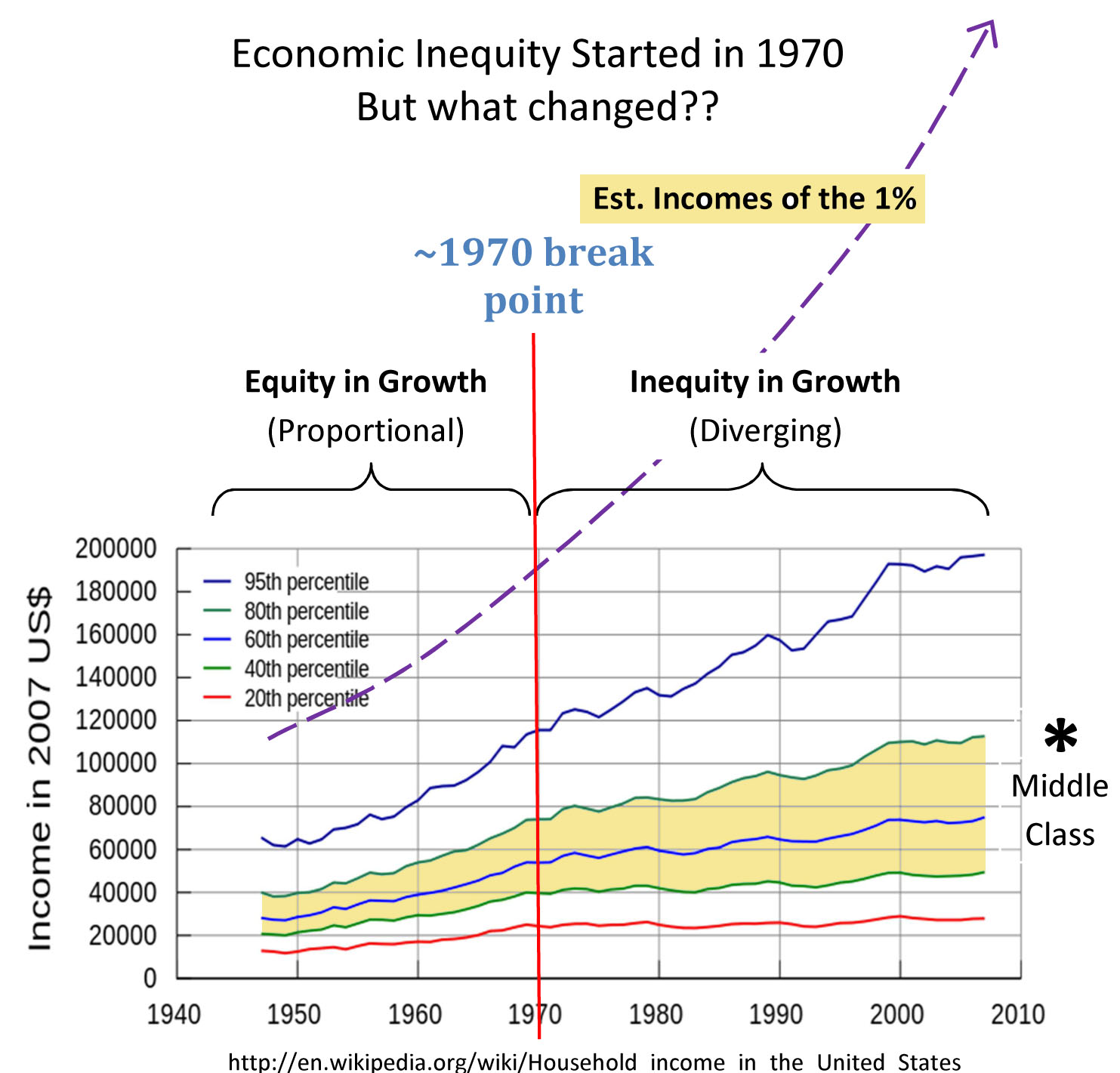

Sometimes local inequities can seem to be blamed on local conditions, but not when it’s a long sustained accelerating global trend. That’s what we see in this US data from 2008, showing that growing inequity in household income has been a very persistent trend. It’s a very familiar subject of discussion and increasing complaint too, that ever increasing shares of the wealth are going to the wealthy. It’s been a central motivation for the UN’s debates on how achieve sustainable development too. So the trend as of 2008, if anything, has probably only been getting worse. Little is likely to change, either, with the SDG’s having no language for reversing the pattern of the wealthy being the only winners in the modern economy.

It’s the household incomes of everyone else that stopped growing.

The US Data for a global trend, of rapidly systematically increasing economic inequity.*

*The estimated trend for “the 1%” is based on US and Global data

showing US & Global GDP having continued to grow as before.

To understand the root cause you need to think about it as a symptom, a symptom of how the global economic system is behaving. The key piece of information is that “What is happening, is happening for the world economy as a whole”. Around ~1970 what happened to the US economy, as the bellwether for the world, is that the wealth of the wealthy kept growing exponentially, more or less just as before. Nothing else did.

The shape of the Data explains the operation of the system

Most of my economic writing revolves around what we inherited, an economic system design for changing faster and faster, exponentially. It’s a dangerous design for which we now have no exit plan at all.

Lots of people mistakenly blame the use of fiat currency for the persistent instability and inequity of the economy. The problem isn’t technically with fiat money at all though… It’s with the deeper compulsion of users of money to use wealth and power as a weapon (we call “investing”), to pay for professional help in taking more wealth and power. It’s the core behavior in question in “the tragedy of the commons” too, that one farmer uses his cattle capital to multiply till the community suffers. Fiat money (basing credit on the value of investments) would actually not be a problem if investors didn’t compound their investments… It’s of course also a broader cultural issue of ignorance about our place in the web of life… but I think the compounding of returns is from what the economy’s growing inequity and disruptions actually originate. I think if investors took care to spend their profits to relieve their demands on the commons when needed then an economic system with fiat money would level out and stabilize.

We need a mid-course correction for the evolution of our economy

What a surprise it will be if to avoid the crises we see coming today, the economy needs a “Circular Jubilee”? It would be a massive effort to give away a great deal of money, very carefully, with the aim of slowing down the economy’s unstable acceleration. Done correctly it would relieve the rapidly building strains we all see, letting us escape from racing the economy ever faster till it fails.

It would be like learning to take our foot off the economic accelerator, to relieve strains and coast a little at the same time. We really need the relief. That really does seem necessary to relieve the economy’s building strains in a lasting way. It would restore society’s resilience and allow us to become more self-healing again too! The design is fairly simple, …to do just the opposite with financial profits as we do now. People would be persuaded to join together and turn away from collecting profits to reinvest in collecting more and more profits. It’s that very widely practiced way of managing money for ever faster growing returns that also sets the course of the economy for changing at exponential rates of acceleration. It has the globally destabilizing results we now see all around.

That traditional way of managing money we inherited is quite untenable in the long term. The one truly sustainable alternative is for investors to learn to spend their profits rather than continually reinvest them! It’s simple math. That’s the the Jubilee part, investors choosing to “release” their profits back to freely circulate in the exchange economy again. The “circular” part is that those profits then freely circulate in the economy again, and return to the investors as sustainable profits. That is the opposite of how we manage our money today.

Today the profits concentrate in the hands of investors at ever faster rates, to only circulate in the economy with promises of being repaid multiplied. It seems to investors that they are becoming more and more wealthy as their world and all its strains increase faster and faster. That’s the fatal path, pushing us toward society’s many possible breaking points. We can do better.

Compounding profits may sound good,

but driving economic change faster and faster

till we are pushed to disruptive and unstable change… is a real problem

((in the diagram, the choice is shown as the alternative between

“$Divested for Care” and “$Invested for Profit”. ))

How the finance economy gives way to the love economy, spending financial profits to earn them back

JLH

(note: first published in 2017 but back dated to 2014, as more consistent with proposals of that time. Using collective profits to care for the commons (rather than for abusing the commons) has been the natural general solution to the tragedy of the commons first recognized by Keynes, and that I’ve proposed in various ways since I first noticed it’s simple necessity around 1979. For more of my writing on it search for my discussions of Keynes.)

New systems science, how to care for natural uncontrolled systems in context