Preface remarks

- This exploration of a pivotal world issue, on which the success or grand failure of our present global development strategy rests… is an example of the wide range of penetrating treatments of important topics covered in the Research Journal “Reading Nature’s Signals“. It document’s Jessie Henshaw’s current application of the the natural systems identification and organizational exploration methods that originated with a discovery in the 1970’s of how transitions in the continuity of natural processes expose the design of the systems and how they are changing, introduced in: The Physics of Continuity = ladders of change

- For more substantiation of this scientific view of how the economy and earth are connected see:

– a Whole Systems view – Piketty’s “r > g”

– A World View of Off-Shore Energy use - For a study of decoupling trends and fluctuation for 1971 to 2017 see

– Evidence of decoupling still zero.

__________

Introduction:

We have a responsibility to use both the words of science and also the methods, when choosing methods of “Sustainable Development” to rely on for our effort to save the earth. It’s often not easy to do. Ask any scientist. It’s often as hard as sitting down to write a great poem, a different kind of creativity but just as demanding. This article discusses the correct scientific method for defining measures of “decoupling” our growing economy from its growing impacts on the earth.

That’s the part of the “Decoupling Puzzle” I can actually answer, offering a way to scientifically define an SDG for Post 2015 “economic decoupling”, and the measure of compliance. See also to the PDF file and XLS file to see the details of the model. It’s a bit different from the approach shown in the UNEP report on decoupling . What I define is an evidence based scientific measure of a growth economy departing form its reliance on growing resource use. It could be used in regulating the economy’s approach of our best understanding of the natural limits of sustainable development:

“A world Decoupling Rate that would assure, within planetary boundaries,

adequate development space and “carrying capacity” to fulfill the intent of the SDG’s.”

How to transform the economy to create growing wealth without growing resource use is left to the reader or other discussions, though I give a hint to what that “entirely new kind of wealth” might be at the end.

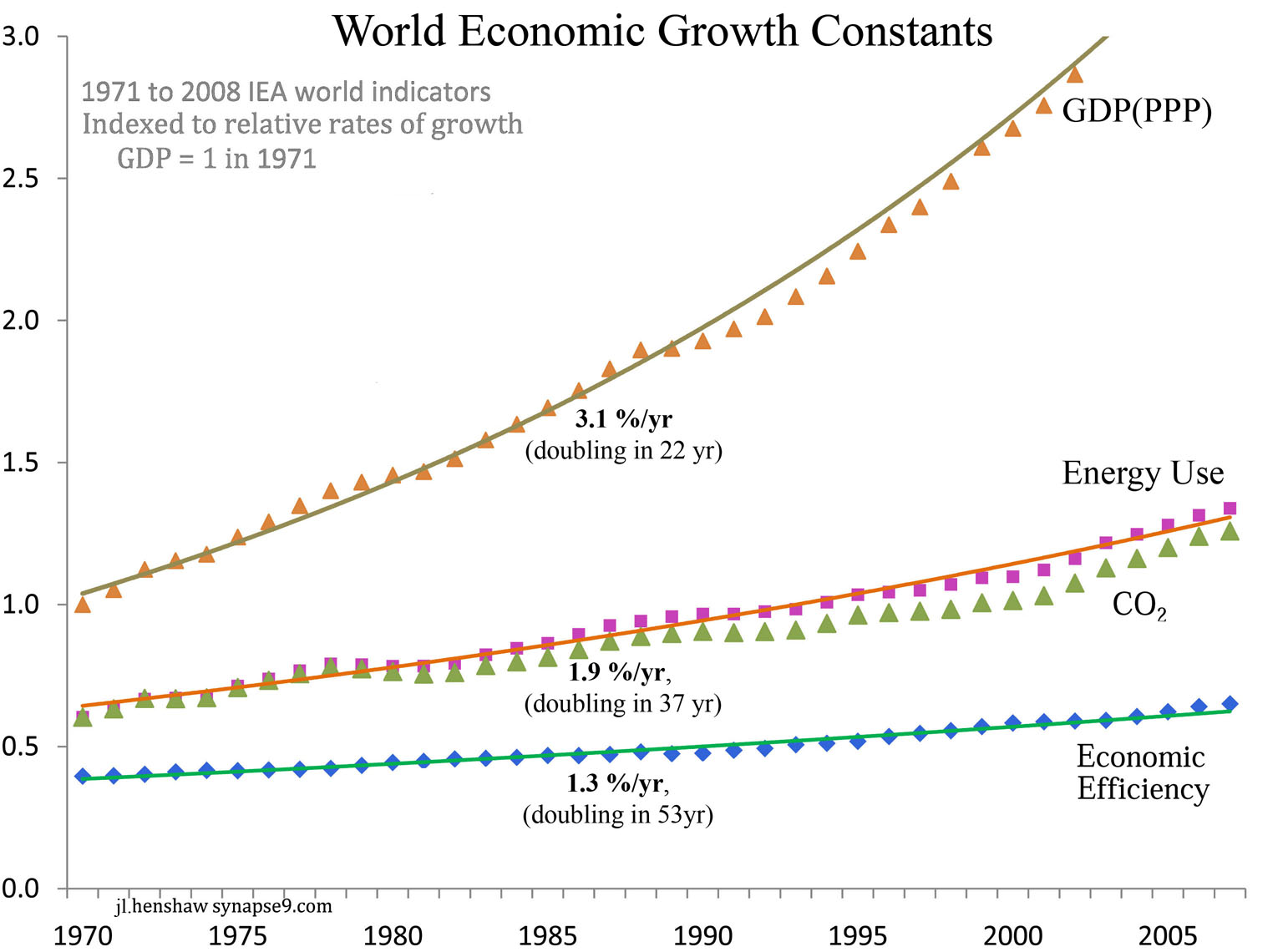

We start with the historic records that display the past “growth constants“ of the world economy. Figure 1. shows GDP, Energy use, CO2 and the GDP energy efficiency of the economy all growing together, with growth rates that are in constant relation to one another. That is the “coupling” of GDP and resource use that needs to be “decoupled”.

That evident constant growth rates and their proportionality (i.e. the “coupling”) is called “natural” because throughout history people have noticed it, tried to explain it, and also tried to change it, all to no avail. This coupling of these measures of the whole economy has continued as if measures of a growing person’s “height and weight”, growing at different rates, but still growing together. It has seemed to be just how the economy works.

As a systems ecologist, myself, I see them as displaying humanity’s natural rate of whole system learning, limited by coordinating all parts of human innovation and development efforts, while struggling to expand at the fastest accelerating rate possible. Systems ecology, then, does not consider economic growth as a “monetary progression” but as an “organizational progression”, a process of “whole society” building on its past to create a new future. This historical record is “how we’ve been doing it” so far, and now that we’ve found it unsustainable we need to change to something different.

…”growth” is a process of our learning how to coordinate doing what we want.

To measure a departure from that we start with the “Economic Growth Constants”:

GDP (3.13 %/yr), Energy use (1.89 %/yr), and Energy Efficiency (1.24 %/yr) . The linkage between the GDP and Energy curves, is the “Energy Coupling Rate” (60.4 %/yr the ratio 1.89/3.13), how fast energy use grows relative to wealth.

The idea and fallacy of “Decoupling”

is to weaken that linkage between earth and economy to zero, changing what has long been a constant coupling rate of 60% by successive reductions to 0.0%, just by continuing to dramatically improve the efficiency of resources use as before. Many people believe new technologies should revolutionize development to do that, other’s think innovation will create products people prefer that just don’t consume energy to produce or to use. What both would agree is that 60% needs to decline toward 0.0%

We could define that transition as a “Decoupling Rate”, the rate at which the Coupling Constant of the past declines toward ‘0.0’. That would allow continued growth in wealth without adding to what we now see are globally unsustainable scales of energy use impacts on the earth. Defined for energy use alone would serve to define it not just for the impacts of fuel extraction and consumption, but also ALL the impacts of a material kind we cause by using the energy we extract for creating economic products.