Today our measures of business environmental impacts address the size and efficiency of business technology use, traceable from local business records. We’re not even trying to measure what’s traceable from what a business pays for throughout the whole economy. So in effect, the global impact is counted within a narrow local boundary, making the measures scientifically undefined, and highly misleading. Why it matters is that business, investor and policy decision makers then don’t know what impacts their decisions really have, and the research says most of any business’s real impacts are global. So we need to understand why the world economy seems to work so smoothly.

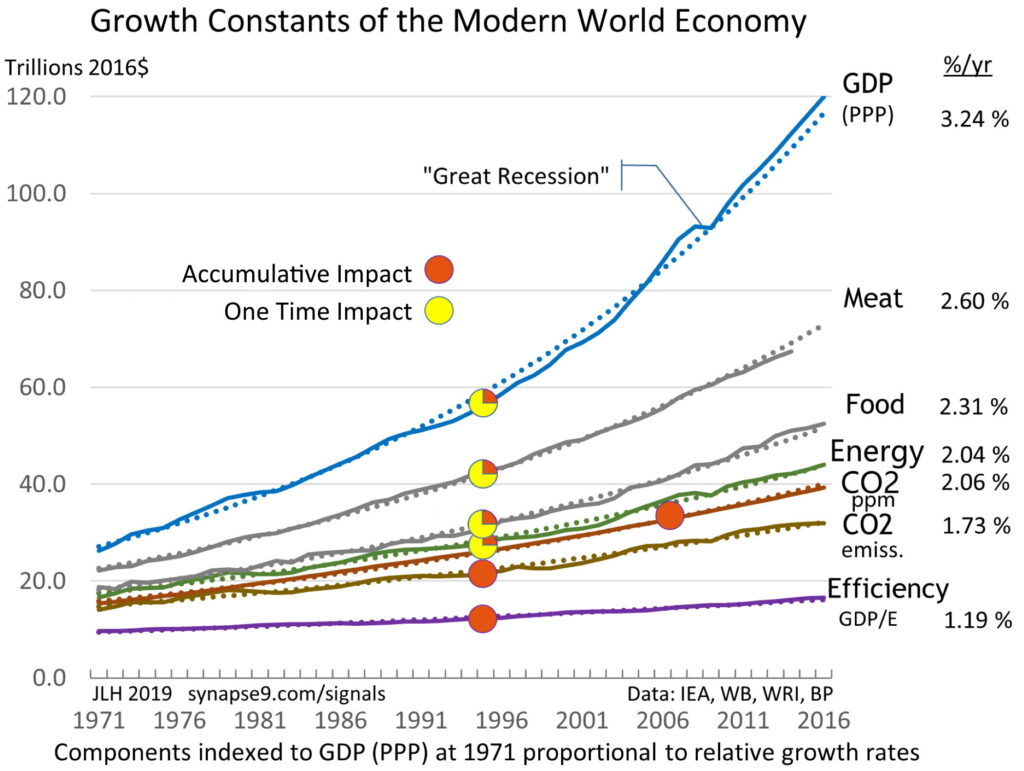

The world economy grows as a whole, as if all parts worked smoothly together, shown since 1970 here, and seems to have for 150 years, hard to imagine but competition seems to assure it, at least for energy use.

What’s counter intuitive for solving it is that the world economy not only LOOKS like a whole system, it also WORKS as a whole system. What you know is 1) all parts of the economy are supposed to be and 2) seem to act as if 3) they are competitively efficient. Otherwise 4) they lose their access to energy use, and the energy goes to someone else. Smooth working competition like that is 5) needed for a world system to work as smoothly as global data shows, and 6) making there no better assumption than that differences from global average efficiency are temporary. So unless someone can say why not, I think we have to treat energy use as being predictably proportional to GDP. That’s been peer reviewed as a general principle, that one can rely on the range of local or international variations being likely to be relatively small (maybe +/- 10%) for any globally connected part.

so…. there’s a LARGE miss-match

between the effects we see and the ones our money really causes

____________

Introduction –

the scientific basis for the SEA-LCA “SCOPE-4” accounting principle,

That: Every dollar spent can be shown likely to pay for such widely distributed services throughout the world economy, that at least as a first assumption, it also pays for an equal shareper dollar of the whole world’s economic activity and impacts. In principle, shares of GDP seem to carry equal shares of responsibility for what the economy does to produce GDP

The worst part of “A Glass Half Hidden” is the clear chance of discovering “An Iceberg of Risks” missing from the view.

Scope 1, 2, & 3 only count the impacts of the primary technology chains that businesses rely on to operate, and ignore the usually much larger impacts of the many chains of business services consumed too. That’s the iceberg of hidden responsibilities of business cause, being ignored due to using an unscientific method of measurement, i.e. counting only the impacts you see, and not accounting for the one unseen (what Scope 4 finally does). So there’s also a hidden iceberg of bigger than expected changes in plan to take care of too… that we’ve been unaware of needing for having a sustainable economy. It explains why our efforts so far still result in the economy degrading of the earth ever faster as we delay making meaningful change. The job doesn’t change, just how directly we’re able to address it.

What’s really hidden is that it’s our money that is directly paying for all the economy’s impacts, making us financially responsible. Now we also really need to know the total bill. Having a habit of not looking at what our money was used to pay for, we’ve been lulled asleep by the way money launders all the information on what our money pays for to deliver what the economy provides.

It is indeed a little ‘strange’ that a very basic scientific principle of measurement, that every scientist knows quite well already, would be overlooked in defining the world’s units of measure for saving the planet.

Scientific ways to measure things, need to measure the whole thing.

Sustainability metrics very largely don’t so that, lacking a scientific way to determine the scale of hidden impacts, the method for measuring economic impacts defaulted to the ancient practice of just counting what you have direct information on. The reality is that the great majority of business impacts actually don’t c come from what is most visible, but from widely distributed uses of the economy that businesses have no records of, paid for by employing all sorts of business services. The problem is that whether you know about them or not, the risk exposure to serious emerging economic liabilities… is exactly the same.

Here’s a new graphic to help picture the problem. It helps to shift from thinking about counting the energy “uses” a business and its suppliers operate with (i.e. traceable for Scope 1,2 or 3, and so on the visible side of the “glass half hidden”), to thinking about the energy uses its revenues are “paying for“, but often don’t have records of (Scope 4, on the hidden side). It’s the total of energy uses paid for that make a business both financially responsible and directly exposed to the emerging economic risks of physically causing economic liabilities and the harms done. It’s a serious major overlooked sustainability business risk. If 80% of the CO2 produced by uses of business revenue actually come from its services, and not its technology,

…it’s all the same to the investor exposed to the risks for the business as a whole.

For risk exposure it’s essential to measure the total impacts on the earth a business is financially responsible for, as that’s where the risk comes from. Just choosing not to count all the ones your revenue goes to pay for moves the risks to the hidden side of the “glass half-hidden”… but still leaves you just as exposed to the very substantial economic risks of business devaluation many see ahead. Continue reading How full is a “Glass Half Hidden”?→

I had found a cozy place to work on sustainability from inside the UN, but discovered the words holding the discussion together there had accumulated meanings that were deeply dishonest… so I’m back on the outside.

___________

Over the past year I developed two rather wonderful scientific learning methods, as if school courses in “Niche Making 101, 102”, for people searching for how to work with nature. One is the 3Step method for learning how your economic commons works and the other the World SDG for making the totality of our growing impacts on the earth transparent to each other. Both were very unexpectedly attacked rather than discussed in the organization I was part of, though, and I’m understanding the offense.

After much suffering, puzzlement and close observation, the harsh reaction to learning by a scientific approach now seems due to it not being sufficiently ideological. Unfortunately… letting up on the ideologies we may use to stamp the world with is the very first rule for learning from nature. Finding that people both didn’t seem to know that, or to be willing to try, is an important lesson I wasn’t prepared to learn, especially that my own social network would respond as if attacked by my suggesting good creative ways to do it .

Ideology is an artificial and inflexible but handy social substitute for reality. By definition ideologies are self-defined, built up as social affirmations in well connected networks. It makes them strong but also largely unable to adapt and respond. For people they provide mental comfort, useful knowledge of group habits, and a private coded language only understood in the network.

How ideologies can open up and become adaptive we often fail to notice, though, how often we naturally change from one to another in the course of a day or week as we engage with different networks. We change ideologies much as if putting on and taking off clothes, often using a change of clothing to do it in fact. So,… it seems sensitive, but need not offend, to notice that ideologies need to be suited to situations and to grow and change with them, letting us try on different ones for fit. Ideologies can be temporarily considered as “nice outfits to wear”, and need not be treated as contracts required of others for whom they don’t fit.

Sadly, the dishonest words this viewpoint helps us understand are some of the favorites in the discussion of sustainability. They’re ways of mixing honorific images of ever accumulating wealth and reducing our footprints on the earth: “sustainable growth”, “decoupling”, “circular economy”, even “sustainable development”. They’re frequently used to compare “apples and oranges” and coming up with “ever increasing consumption without consumption”. With that usage our goal and purpose becomes to accelerate the “tragedy of the commons”, that is our whole discussion is about how to avoid.

How you can tell that for yourself is by observing that putting the contradictory meanings of “development” together requires switching back and forth from one ideology to the other, with that switch not being mentioned. It shows that people, in conversation, are adopting an ideology of hiding when they switch ideologies. Sadly that seems what we have socialized around doing, unaware of the consequence. At present nearly anywhere in the global sustainability movement you go (and I’ve really looked around!), you get strong pushback for even trying to bring it up.

The natural succession of growth and adaptation for sustainable systems, a complex organizational development of internal and external relationships.

Nature doesn’t respond to artful ideology in the least, though. Not one little bit. What nature responds to is the growth of new organisms that change from expanding their conquests to then making their niches. That succession is their (and our) door to joining the commons by making their (and our) homes in it. Feel good euphemisms for the opposite, stitching together our true ideals into fig leaves for endless conquest philosophies like BAU, actually don’t work.

No need to take off our clothes in public… but dropping ideological fig leaves at times

seems required for how we learn.

Offering a true measure of economic sustainability, internalizing the costs of externalities caused by delivering world GDP, initially using shares of GDP to measure shares of GDP impact responsibility; potentially making the world economy 100% accountable.

It’s the “right way to make money”, taking responsibility for the true shares of our costs to the future.

Investing and doing business in the common interest,

…calls for balancing costs and benefits, no longer just counting operational impacts locallyas before, adding up only the impacts over which we have direct control (and can’t hide). Now we need to do impact accounting inclusively, combining in one account both direct operational impacts and direct economic demand impactsestimated as our global shares of the GDP impacts we pay for. That’s the essential step to inclusive accounting, and balancing our benefits from GDP with our real shares of responsibility for the whole economy’s accumulating GDP impacts. It’s needed to guide our choices for moving toward a sustainable future.

To apply it we need to recognize that the supply-chain and service-chain impacts are a *shared responsibility* of the those managing the operations the result from, and the economic demand caused by paying for them. Now the World SDG offers a scientific method for measuring the responsibility of economic demand. Businesses and investors need to make sound sustainable decisions about supply chains reaching around the world, and need accurate information on what is being paid for and profited from to do that. Consumers, shareholders and regulators can then also make sound decisions about what the markets are profiting from. For the glaring cases, regulators could variably tax the profits from dangerous impacts, funds to be transferred to subsidizing the profits for scaling up alternatives, making the investor and buyer jointly responsible with the seller for the important side-effects of their economic services. In principle both buyer and seller are co-equally responsible, liable for long term costs of short term profits, and for being transparent. This way of doing the accounting would help pave a clear path ahead for the economy of the future. 06/26/17, 11/5/18

______________________

Updated Preamble to the 2014 UN Proposal

Following these notes is the original text of the World SDG proposal, to the UN Ministerial “Open Working Group 7” and the UN NGO Major Group and its Commons Cluster, for negotiating the global Sustainable Development Goals (SDG’s). It offers a “whole system accounting” method to give all stakeholders the same transparent information on measurable Environmental, Sustainability and Governance (ESG) impacts of the economy, to help guide economic choices for our future. What makes it work is a new scientific method for much more accurately distributing real responsibility of economic decision makers for their decisions. That new science, for how the world economy works as a whole, is what allows all stakeholders to see their own and each other’s real scale of impacts on the whole caused by their economic decisions. It becomes a learning tool for then guiding our choices for the benefit of the whole, creating a holistic awareness of what’s at stake for consumers, business, investors and governance, and guide efforts for achieving the SDG’s.

Latest 2016 research statements, The links below are to recent UN Statements regarding how our standard ways of measuring sustainability are very selective, and leave the great majority of economic impacts on our future uncounted[1,]. My recent video comment to the UN [2,] on this grand accounting problem is in the webcast of its high level political policy forum for sustainable development (HLPF), its July 11 Session 4: Fostering equitable growth and sustainability . Watching the hour of statements from many experts, countries and organizations will show you how the UN works, and avoids discussion of our ever expanding impacts. My statement is at minute 0:40:40, and others by Youth, Women & Indigenous Major Groups are at minute 1:09:00 to 1:21:00, and quite excellent too.

Our modern environmental accounting standards were based on ancient habits of not counting things we can now measure the effects of. The is largely limiting the information given decision makers to LOCAL impacts, and leaving uncounted their real shares of the GLOBAL impacts. These categorical omissions from what is counted assure that businesses, investors, government and consumers will make sustainability decisions quite unaware of most of the impacts their decisions will cause. What is excluded also tends to be the more neglected and disruptive of our accumulating economic impacts on the earth and society, and so excluding consideration of them in making the decisions that cause them. So sustainability decisions to maximize profits can also be maximizing neglected impacts too!!!

We’ve never had a meaningful balance sheet for the earth, but new science and technology now makes it possible. Our accounting methods started from doing local accounting of impacts, and so didn’t take a whole system view, and that’s still the case. So leaving them out of consideration means it’s only slowing the whole economy that slows its increasing whole effects that are continuing to destroy the earth.

I) The standard way ‘sustainability’ is now measured uses “selective accounting” rules, for addressing ESG impacts, for people, businesses, cities or countries or policies. It’s to count things almost entirely only for what each one directly manages. That counts what each planning group would immediately care about, but it ignores the often much larger remote effects of their commerce on others and the planet, a very deceptive one sided view. For businesses energy use, for example, what is counted is only the energy within its operations, for its equipment and the material uses it manages, or directly traced to them. Even though doing that takes a great deal of effort, it arrives at a total that is highly inaccurate and misleading, due to the more dispersed categories of impacts uncounted.

II) The most general exclusion is of all impacts of financial choices, all treated as ‘zero’, though also very clearly resulting in what is paid for and profited from, by consuming all the services of the economy remotely. The largest part of that exclusion is the financial choice made by businesses to pay their own people, and so economically causing the consumption. Business use of public and private services, and paying investors are also excluded. Also excluded are all those categories of paid services impact for business supply chains. So given that we are now relying on environmental accounts for saving the earth, it’s evident that no one before had been checking what decision makers would be told they were making decisions about.

III) To make real decisions on sustainability decision makers would need to accept co-equal responsibility for their choices to request, pay for and profit from their share of impacts for delivering their share of GDP. Because our responsibility for what we see happening around the world is not traceable you need to count it statistically, and the new research makes that relatively easy. It gives co-equal responsibly for directing the work of a business supply chain with the operations of the supply chain.

The original research (3, 4) found the whole supply chain energy consumption and CO2 pollution of 5 times what the Life Cycle Assessment (LCA) or GreenHouse Gas (GHG) “Scope 1&2” metrics would count, using a wind farm business with heavy technology as model. For less for businesses using less heavy technology, the true impact might be 10 times what is counted, with the more disruptive remote impacts going completely uncounted. The old rules were inherited from practices for simplifying accounting and ignoring things that were hard to count. It reflect the oldest of old habits of thinking, of economies working with separate parts, when since Adam Smith everyone has known they work as a whole.

IV) The World SDG proposes a data network giving access to a transparent inclusive accounting of measurable ESG impacts, a data platform. The starting point is a scientific method of dividing up shares of known impacts of the whole economy, for which any part would be responsibility. The baseline for estimating a share of economic responsibility is the decision maker’s share of the economy, initially counting every share as “average”, and then differentiating if more information is available. So as an impact calculator, any person, business, or country would enter their “income” and first see a display of the known global impacts for that share of world GDP. It would be for helping them choose how to invest their time and money, and guide policy. As research develops, ways to depart from average and take credit for lessening or compensating for impacts would develop.

The principle strategy for the World SDG is to improve the decision making regarding investments, thinking of “investment” more holistically, as both “cultural development” and trying “new directions for the economy”. For operating businesses its ESG balance sheet report would be published along side its annual financial balance sheet report. All stakeholders could view the same “best available information” on all impact factors. When a new investment proposals want public recognition and perhaps qualify for support, they’d go through public reviews. First would for general scientific and economic feasibility, then financial, and then for cultural acceptance and political commitment. From initial to final reviews it would proceed as a “learning practice” going from early concept to final implementation stages. More successful proposals might be seen as “transformational” and become a teamwork of all the stakeholders, not just the initiators.

Our main sustainability impact metrics (2)

LCA (Life Cycle Assessment) accounts for the impacts of recorded uses of technology and materials by individuals and businesses

but not the impacts of OTHER spending and economic choices

EF (ecological footprint) measures our traceable use and flows natural and renewable resources

also not the impacts of OTHER spending and economic choices

The World SDG method combining the omitted economic impacts with scientific measures (3)

EI (economic impact) measures accumulative responsibility of participants in the economy for shares of global ESG impacts of GDP, assumed to be proportional to shares of GDP until improved information is available.

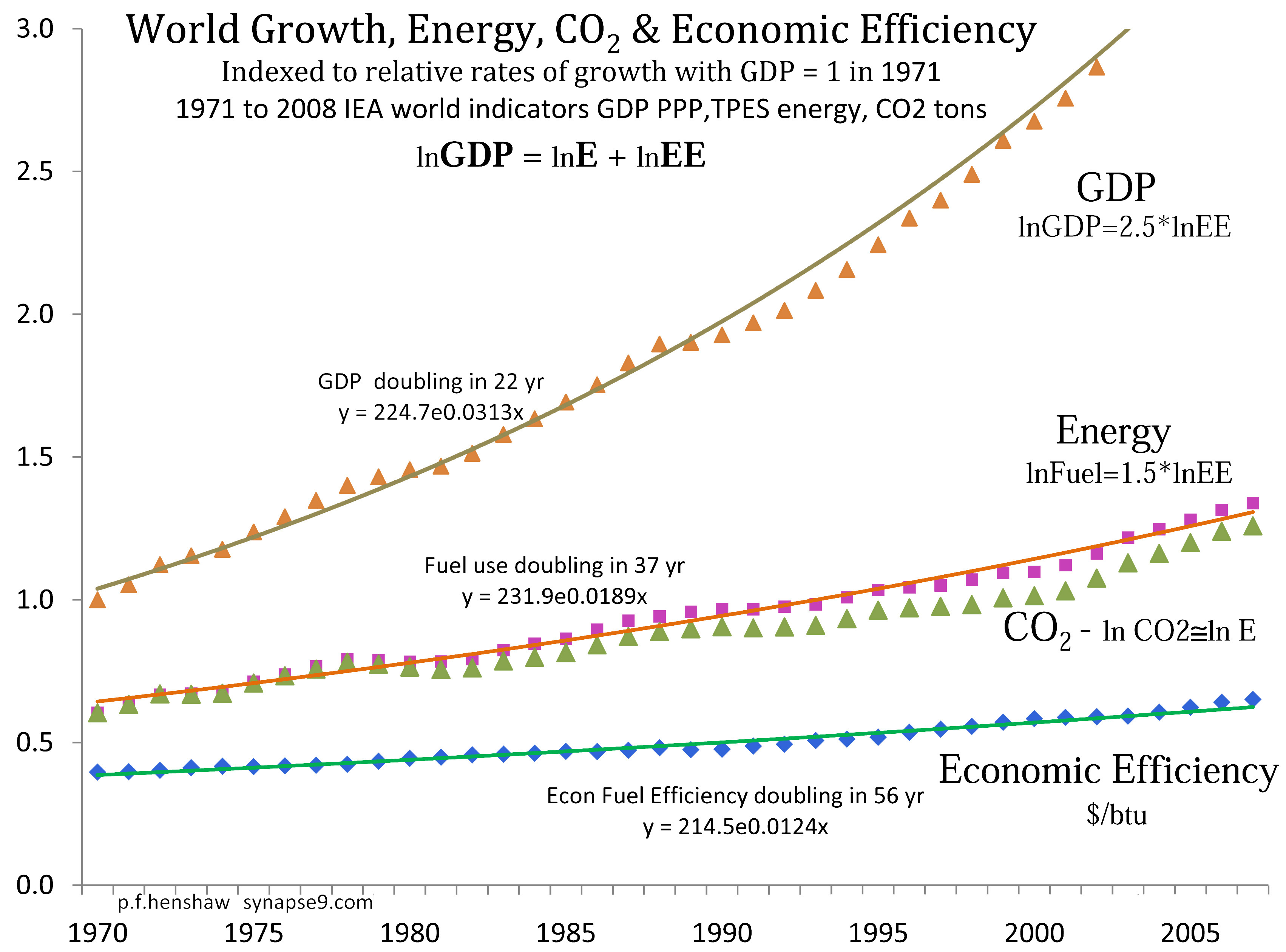

Share of GDP is a reliable measure of our use of the economy, on the currently reliable assumption that the measured economy works as a whole, based on the highly regular relationship seen in the first figure below, of a constant ratio of constant whole system growth rates for GDP, Energy & Energy Efficiency. Also see the Addendum – Background on the Science and references (4, 5a,b)

______________

Preface

Why a World SDG is both possible and needed is because our world economy works as a whole. We need a truly global way of understanding the impacts of our decisions, to crate a “Knowledge Commons for Sustainability”. We recognize that every part contributes to the whole and no part can operate without the whole. The surprising result of the research is how reliably any share of GDP is likely to be “average” and pay for about the same share of world GDP impacts (4). 1) It first comes from how widely distributed consumption spending is, then 2) how widely money from any expense is distributed in the global economy, to all income levels within all kinds of businesses, as it is passed down a supply chain(5a,b). It then also relies 3) on how truly global and competitive economic markets and services are, with all parts being disciplined by the same competitive standards for profiting from the resources everyone has access to. So the baseline assumption that shares of GDP pay for the same average share of GDP impacts is both necessary as a default choice and likely to be accurate. Making decisions on how individuals and the world can depart from average would then become the focus.

Everyone could then understand their own benefits from the economy and how they compare with the global impacts of delivering them, seeing the simple facts in a broad context. For example, a 6 oz (180 cc) glass of wine for $10 seems like a small impact. As an average share of GDP what we find is $10 is quite likely to have an “average climate impact” of .45kgCO2/$ = 4.5kg for $10 = ~10lb x 16oz = 160 ozCO2 [2006 data] (4). So the weight of CO2 consumed would be ~27 times the weight of wine. The catch is that spending $10 on anything else would be the same. How we use any part of our incomes would be close to having an average share of CO2 AND other global impacts of the economy as a whole, soil loss, deforestation, environmental and cultural disruptions etc. [for 2016 data due to inflation and efficiencies impacts per $ are ~66%]

So the World SDG accounting model lets you:

Compare our shares of World GDP benefits with our shares of its measurable Ecological Societal and Governance (ESG) impacts.

Using “shares of the whole” as a common unit of measure for responsibility for the whole

by aggregating reliable measures of human impacts and risks to our future, including direct financial liability if there are good estimates

using the sound initial baseline assumption of “average responsibility per share” pending more complete accounting.

It would provide an accurate accounting for the modern world’s survival on earth. [ed 8/23/16]

… a scientifically combined balance sheet for financial and ESG factors, so people can better understand our economic choices.

___________________________

.

A World SDG

A World SDG is a “commons approach”

Full accountability for the rising economic costs of an unsustainable future

Finance motivated to invest in the SDG’s close to our hearts.

An integrated balance sheet of local and global responsibilities for integrated implementing of SDG’s.

New science makes it possible to give those who profit from growing our costly economic impacts the information they’d need to understand their growing global liability. What would be more profitable choices for all can then reverse that. It’s shocking, really, when one finds what a $1 dollar share of GDP (where the averages apply) is responsible for, as a $1 share of today’s economy’s fast growing impacts. Every average $1 of GDP is responsible for close to 1lb of CO2 put in the atmosphere! So in a sentence you just replace “dollar” with “pounds of CO2” to speak about the climate impact of normal earning and spending. For a consumer with a $50k income, the climate impact is 50k pounds of CO2 per year!

Parallel growth rates for world GDP, Energy, CO2 and Efficiency => make average shares of GDP responsible for the same share of those parallel impacts.