How about if you made it fairly realistic, allowing money holdings to continue growing normally even when the amount of product doesn’t, as it we have now. Keynes proposed his change in the rules for that circumstance, for how to coordinate the emergence of “peak stuff” with a matching “peak money”. Do you think it would be worth designing a money game to see what winners would do with their multiplying ownership of finite goods in that case, and if they’d discover the way out? Continue reading “Distoppley”, the game after “Monopoly”→

3/15/10 This is an edited foreword for my 3/13 post and a P.S. It’s really about deflecting the false impression made by an unfamiliar view of historic data, so not of general interest, I think.

A recent note came from Charles Hall, with two interesting things. He passed along thePeak Oil Review pointing out again how oil prices are edging upward even as the economy slips. Continually rising prices is a natural symptom of trying to grow with diminishing resources as I offered a theoretical basis for in “Profiting from scarcity” last year.

Then he mentioned a provocative series of graphs from Nathan’s Economic Edge. These are graphs of first derivative rates, with the one below showing rates of increase of US national income fluctuating wildly as “steady growth” has been frequently broken by recessions. It also gives an impression like the increasing roller coaster experience of keeping up with economic change.

The real question is why would the irregular rate of economic growth remind us of the increasingly desperate struggle it has been,

Nov 2013 note: Since this popular post was written I’ve kept pushing my search for better explanations. It’s basically a very simple universal principle for how growth leads to stability. Every successful ‘project’ in nature, of any kind or scale, starts with using its resources to build more access to resources, expanding on itself, and then stabilizes by changing its strategy before it is overbuilt. It’s easy to recognize that turning point in one’s own projects or new relationships. It’s that point when you “have enough to manage” and can turn to bringing it to fruition, not taking on more for seeing good reason to secure what you already have. Taking on more for no reason would threaten what you began.

As a shift from taking territory to homemaking

Your self-investment strategy begins with searching for how to expand on a great beginning, using gains to expand your gains, and is uninhibited at first. It’ll only succeed if sensitive to the approaching need to stabilize and switch to “homemaking”, and creating a secure “niche” in the environment for what was built. What changes in the investment strategy is its “targeting radar” for the best use of its resources.

As the organization is built up it first prospers by expanding its control of its environment, creating new internal organization and overhead costs. The value of building by bigger and bigger steps (creating more overhead while depleting the availability of resources) naturally reverses. Then like homemakers who “see success in sight”, the radar shifts to caring for what they built as a whole and that “near environment” it needs to be secure. It’s a switch from taking territory and building bigger things, to caring for how things fit together and work smoothly throughout the whole, from aggression to caring.

____________

Mar 12 2010: Twenty-five years ago I learned that Keynes had come to the a similar conclusion I then had had, about how to achieve a stable steady state economy. At the same time I found out Ken Boulding, the leading economic theorist and leader of the General Systems Theory community, had been talking about it for decades after Keynes too. But their efforts had gotten culturally buried.

Because it was pure systems ecology, without any cultural roots in the business or finance community, his proposal seemed utterly radical. He first called it “the widow’s cruse” after a biblical story about Elijah giving an old widow an inexhaustible cup of oil and bowl of flower (1, 2).

How natural systems can remain profitable at limits to growth.

Keynes’ had realized that capitalism would produce an over-investment crisis when the environment started producing diminishing returns. At that time acting to stabilize growing investment, as his main work had been about, would destabilize the economy as a whole.

The real crisis would come from those with wealth continuing to increase their investment savings and so multiplying their investments and demands on the productive economy for growing returns. The Increasing demands on the non-growing economy would then undermine the economy’s profitability to the breaking point.

It was called “the fallacy” by everyone around him, though, and so it broadly remains considered today, by the few who know of it.

The way social customs develop, and community standards, what to expect is formed by agreement and not by research all the time. Then people teach what others before them agreed on.

I think that could be the main reason why for a few hundred years everyone assumed the right thing for economies would be regular % change just because everyone wanted steady improvement. It seems the effect of multiplying economies on the earth was never really studied, but just whether it to fix the problems that arose or not.

As a physicist in the mid 70’s I was watching the curiously creative behavior of a lot of uncontrolled natural “economic systems”, heat transport by convective currents inside buildings. I spent a couple years doing of 24hr micro-climate fingerprints of buildings, closely studying how their air current networks competed for flow channels and evolved new organization several times a day as the sun moved around.

Sometimes it pays to recognize circular arguments with no escape, and realize one or more of the core assumptions causing that needs to be questioned.

The presently brutal and worsening job market in the developed countries is often discussed with a circular argument: that stimulus isn’t working so we need more, but governments run a risk of collapse if the jobs are not productive… That is now heard over and over, and it’s worth looking at it as painting a circle of common assumptions that everyone would like to escape.

The problem caused by economies becoming unresponsive to Keynesian stimulus was actually brilliantly studied by Keynes… His simple conclusion was that when stimulus provided by governments filling in as “spenders of last resort” didn’t work then investors would need to take that role, even to the point of ending the accumulation of investment to make economies physically sustainable. The assumption that is not variable is that we live in a finite world. Continue reading Switching the “spender of last resort” when government goes broke…→

How we can reduce our negative impacts on the world is by finding the right question to ask.

Choosing the right things to spend on doesn’t really do that, for two very good reasons.

Most money you spend will have about average impacts per dollar anyway. If you think where money goes and how each product takes so many kinds of inputs, every dollar really uses the whole economy, and on average, now produces about 1.0 lb of CO2!

Because it generates profits it also stimulates economic growth at around 3% a year, made possible by a similar increase in what we are trying to take control of in nature, per dollar. So buying expensive “green” products does more harm than cheap products by having nearly the same average impacts throughout the world, per dollar. You could buy cheaper products, but because you’d then buy more there’s no escape… either way.

The real trouble with understanding your own accumulative effects on the world is that the human theory of cause and effect, like pool balls bouncing around transmitting effects from elsewhere, isn’t the way nature accumulates effects. Bouncing balls is not the glue nature uses, you might say.

The effects of pressures and forces are real and all, but they nearly all dissipate as they bounce around, rather than accumulate. So…our usual idea of “cause and effect” simply does not apply. That’s a key reason for why good intentions often don’t have their intended effect…

I think the answer is, well, yes of course… Most people seem to

intuitively confuse increasing their access to resources with increasing the

supply when increasing their access to resources actually decreases the earth’s

supply.

This is another way to understand the various mysterious efforts

to reduce the impacts of growth by streamlining and accelerating growth, which

of course multiplies its impacts. It basically means we are not being

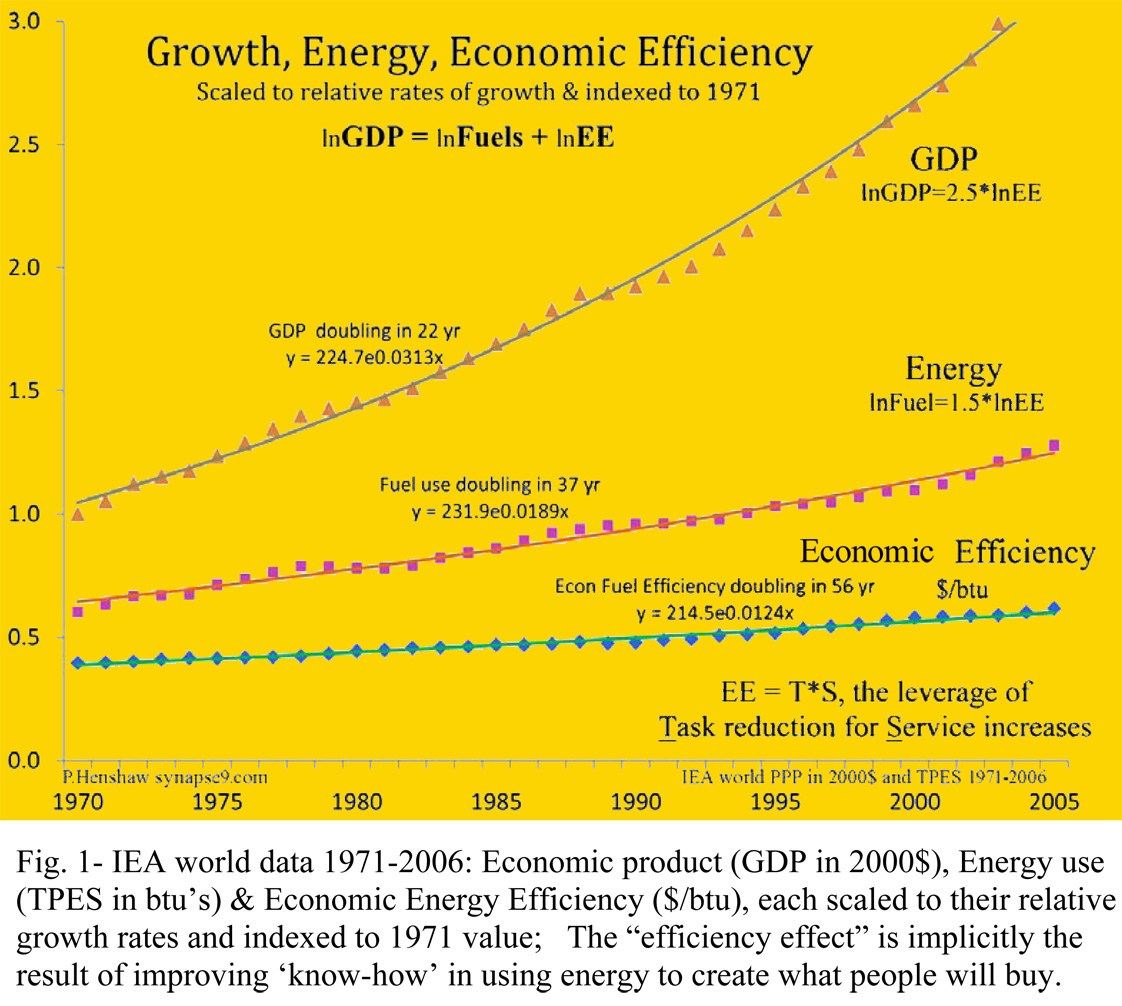

self-critical and asking the hard questions. The easiest data to display the

effect with is the world energy/GDP balance:

Phil,

[I was] just looking for smart people to join our group. After checking out your site, I believe you may be overqualified. Your stuff is brilliant. I found this portion on the market pundits fascinating, from The Bump on a Curve Notepad:

“Well, I’ve been wondering for a long time why the flows of change are so hard for people to see, and do think there’s some kind of “fixed world illusion” to contend with. There’s a list of reasons why we don’t update our information regularly and so miss the flows of change because of that.

It’s a little speculative, but another detail caught my attention recently, that even when repeated changes in “normal” are quite dramatic, people often only have to “sleep on it” to readjust and see even very short lived situations as if they were permanent and a brand new permanent “normal”.

Nearly every pundit and media source from 2007 to the present has radically changed their stories about the economic collapse nearly every week… for example. They always seeming very comfortable with the “ever present” finality of their quickly changing stories. It’s like there’s a “reset button” that they all keep using, in their sleep, that completely hides the facts of accelerating change. Continue reading Noticing change, through the fixed world illusion→

New systems science, how to care for natural uncontrolled systems in context