Re: Annie Leonard’s brilliant work in the “The Story of Stuff“, and the hiding places where nature puts some of the missing stuff.

+++

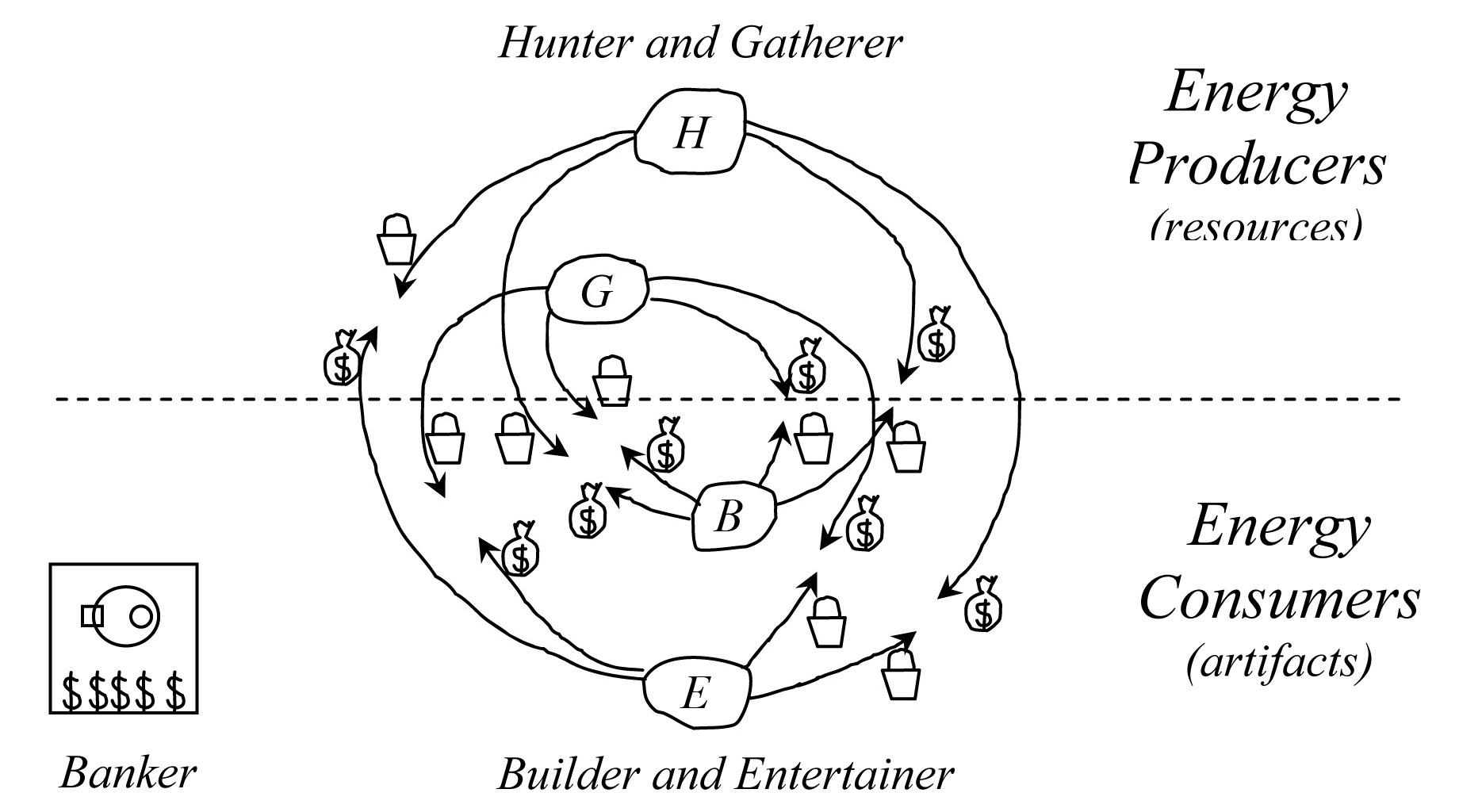

Annie, Hi, great work, I’ve always admired it. I’m a natural systems scientist, and… there’s a whole LOT of “missing stuff”. Closely studying the mystery of how nature organizes things into “whole systems” has a secret power, that any one part can lead you to… layer upon layer of the missing stuff. We should have a lot to talk about, but catching your attention is a difficulty these days.

Most people assume that once they’ve found one answer to a question, that’s it, and there’s nothing else to look for. But oh no, that’s usually the beginning not the end. Like, people see 1 thing wrong with money and think fixing that fixes every thing that is wrong with money. Nope, you have to look at things from ALL sides to find ALL the gaping holes. Just patching up the first thing that comes into sight isn’t enough. After a stumble you may tie your scarf and in a hurry “look smart”, but not notice you’ve been sitting in mud! Continue reading The story of the Missing Stuff

(1)

(1)